- Share

-

-

-

Check the background of investment professionals associated with this site on FINRA's BrokerCheck.

Many things in life get simpler when you retire, but unfortunately, your finances aren't one of them. If you're like most people, you'll rely on multiple sources of income during retirement—Social Security, pension payments, 401(k) plans, personal savings, even wages if you start a new career or work part time.

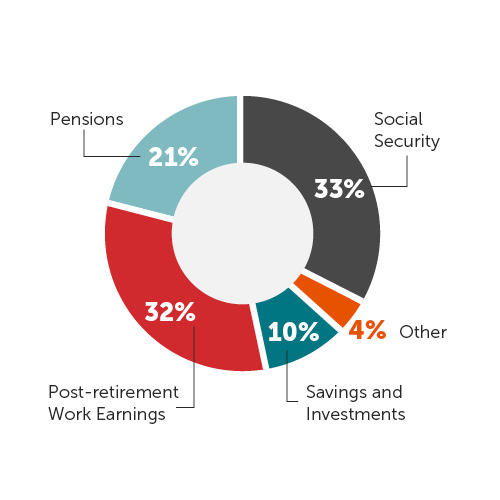

Retirement Income Types

According to the Social Security Administration, 85% of American's retirement income comes from Social Security, Pensions and income earned post retirement.

Social Security (33%)

40% of people have to pay taxes on their Social Security benefits.i The taxable amount varies based on your combined earnings and filing status, up to a maximum of 85%.ii

Post-retirement Wages (32%)

Half of workers age 60 and older plan to keep working until at least age 70.iii No matter how old you are, if you work, your earnings will be taxed.

Pension Payments (21%)

Payments from private and government pensions are usually taxable as ordinary income, assuming you made no after-tax contributions to the plan.

Where America's Retirement Funds Comes From

You'll also have to pay taxes on your retirement income. Since different income sources have different tax implications, it can get complicated. To strive to avoid paying more taxes than you need to during retirement, you'll need to familiarize yourself with how different types of retirement income are taxed.

Taxable Retirement Income

Tax-deferred Accounts: 401(k), VIP, 403(b), Traditional IRAs

Withdrawals of pre-tax contributions and all investment earnings are taxed as ordinary income, so think twice before tapping into tax-deferred savings. These plans are also subject to Required Minimum Distribution (RMD) rules once you reach age 72, and there are stiff penalties for failure to do so. (Prior to 2020, these plans were subject to RMD rules at age 70 1/2.)

Interest and Dividends

Interest from savings accounts and CDs, and dividends/interest from taxable money market mutual funds and brokerage accounts are taxed as ordinary income.

Capital Gains on Investments

Profits from the sale of assets—stocks, bonds, mutual funds, even your car—are taxable. If you owned the asset for less than a year, you'll pay short-term capital tax at ordinary income rates. Long-term capital gains rates are more favorable. The maximum tax rate is 20%, but most taxpayers pay zero-to-15%.iv

Non-Taxable Retirement Income

Social Security

If Social Security is your only source of retirement income, or if your total income falls below certain limits, chances are good that you won't pay taxes on your Social Security benefits.

Tax-deferred Accounts: 401(k), VIP, 403(b), Traditional IRAs

Withdrawals of after-tax contributions from 403(b) plans, 401(k) plans, Traditional IRAs and other tax-deferred retirement savings plans are not taxable. RMD rules and taxes on gains would still be applicable.

Roth IRAs and Roth 403(b)s

As long as the Roth has been open for at least five years, and you're 59½ or older, all withdrawals are tax-free. Unlike traditional IRAs, you don't have to take Required Minimum Distributions from your Roth.

Municipal bonds and mutual funds

These sources of income are tax-free at the federal level.

Other Factors Affecting Retirement Taxes

Aside from how your retirement income is taxed, there are other things you'll want to factor into your retirement tax strategy. Among the biggest changes you'll need to plan for are:

Required Minimum Distributions

Annual mandatory distributions from tax-deferred accounts such as 401(k), VIP, 403(b) and traditional IRAs begin when you're 72. That additional income is significant and could push you into a higher tax bracket. The penalties for not taking RMDs are severe: 50% on the amount of the required distribution.

Quarterly Income Taxes

When you're getting a paycheck, your employer takes care of tax withholding. But when you retire, you're responsible for paying your taxes as you go. Most retirees need to make quarterly estimated tax payments—and do the planning and calculations necessary to correctly estimate quarterly tax bills. Failure to pay estimated taxes, or not paying enough, could result in a penalty from the IRS.

Retirement Income Tax Tips

There are many things you can do to manage overpaying taxes when you retire. While everyone's tax situation is different, here are some options:

- Diversify your retirement income sources for more flexibility.

- Take distributions from tax-deferred accounts while you are in a lower tax bracket.

- Convert some tax-deferred dollars into a Roth IRA, if appropriate.

- Hold off selling investments until you've owned them at least 366 days to take advantage of lower long-term capital gains tax rates.

- Ask your financial advisor to use tax-harvesting strategies to offset capital gains with capital losses to manage tax impact.

- Have your broker or financial advisor withhold state and local taxes from any distributions or payments you receive to avoid having to pay estimated quarterly taxes.

Start planning your retirement tax strategy now

Managing your taxes in retirement is complicated—and mistakes can be expensive! Fortunately, you can manage costly missteps with careful planning. The most important thing you can do is to create a retirement tax strategy before you retire. Once you are retired, you'll need to stay on top of withdrawals to make sure you have the money you need while aiming to keep your taxes low.

Questions?

Financial Advisorswith BECU Investment Services are here to help. They can work with you to develop a detailed retirement tax strategy and withdrawal plan that's appropriate for you. Set up a complimentary consultation or call 206-439-5720.

This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

Contributions to a traditional IRA may be tax deductible in the contribution year, with current income tax due at withdrawal. Withdrawals prior to age 59 ½ may result in a 10% IRS penalty tax in addition to current income tax.

The Roth IRA offers tax deferral on any earnings in the account. Withdrawals from the account may be tax free, as long as they are considered qualified. Limitations and restrictions may apply. Withdrawals prior to age 59 ½ or prior to the account being opened for 5 years, whichever is later, may result in a 10% IRS penalty tax. Future tax laws can change at any time and may impact the benefits of Roth IRAs. Their tax treatment may change.

iSocial Security Administration. "Understanding the Benefits (.pdf)." 2018.

iiSocial Security Administration. "Benefits Planner (.pdf)." 2018.

iiiKimberly Palmer. " Is 70 the New 65?" AARP. March 31, 2017.

ivInternal Revenue Service. "Helpful Facts to Know about Capital Gains and Losses." April 2018.

Financial Advisors are registered with, and Securities and Advisory Services offered through LPL Financial, a Registered Investment Advisor, Member FINRA/SIPC. Insurance Products offered through LPL Financial or its licensed affiliates. BECU and BECU Investment Services are not registered broker/dealers and are not affiliated with LPL Financial. Investments are:

BECU Investment Services Corporate Office located at BECU, 12770 Gateway Dr., Tukwila, WA 98168. BECU, BECU Investment Services and LPL Financial are separate entities.

The LPL Financial Registered Representatives associated with this site may only discuss and/or transact securities business with residents of all 50 states.