How To Get a Credit Card for My Kid

Even though kids younger than 18 can't get credit cards of their own, parents still have options to use credit (and debit) cards to help their kids enjoy a bright financial future.

Reasons parents want to get credit cards for their children vary. Maybe you want to jumpstart your kid's credit. Or maybe you want to teach them about budgeting, saving and spending money. Or maybe you just want to give them a way to shop without carrying cash. Having a clear idea about why you want your child to have a credit card can help you make the best choices for your family.

Comparing Kids' Credit Card Options

Different types of credit and debit cards have varying features that can help you accomplish different goals. These come with different levels of responsibility for you and your child, ranging from all the responsibility on the adult to all the responsibility on the child.

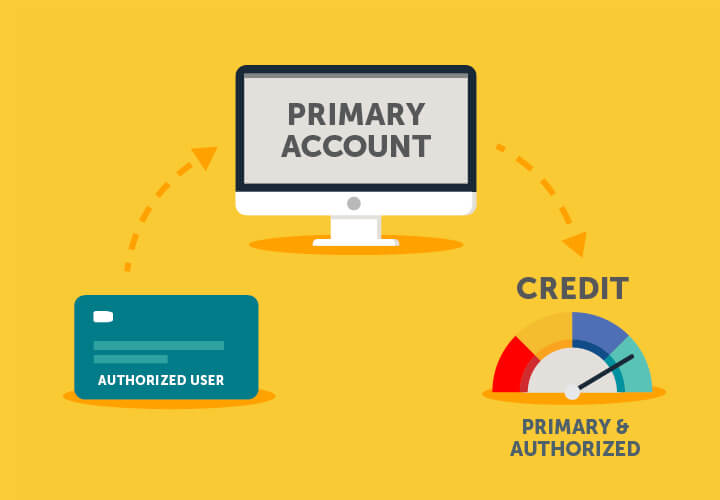

Authorized User on Parent's Credit Card

The easiest way to help your teen get a credit card is to add your under-18-year-old as an authorized user to your card account. Different card issuers set minimum age requirements for authorized users. For example, BECU asks authorized users to meet a minimum age requirement of 13 or older. However, as the primary cardholder, you remain responsible for ensuring the card is paid on time.

If you make your teen an authorized card user, a card with your teen's name will be mailed to your home. Charges on the card may be reported to the credit bureau for your child's file and help to build credit. Depending on the card issuer, the child may be able to log in, review their own charges, and make payments, depending on the card and issuer. BECU authorized users can't do so, however.

The authorized users' card is the same number as the account holder's card, explains Meghin Margel, director of BECU's lending solutions. "The holder gets the bills, applicable cash back and is responsible for the payments," she said. "But it's a great introduction to credit and a credit-building tool for the authorized user."

An authorized card gives you the chance to teach your child valuable money lessons, including:

- Good credit habit: Budgeting and how to set spending limits.

- Bills: How to read a credit card bill.

- Monthly payments: Making regular, timely payments.

- Credit usage: Spending less than 30% of their credit line.

- Interest: Why and how interest payments affect how much you owe.

Ask the card issuer if it reports the authorized user to the credit bureau — a card could help your child build a future credit history, too.

Pros of Adding an Authorized User

- If the card issuer reports the authorized user to the credit bureau (some don't), your child's credit history after turning 18 could reflect the payments and amounts owed.

- Provides you with a chance to oversee your child's initial card use and discuss money and debt management. You may need to pay close attention to card statements for both of you, for a while.

Cons of Adding an Authorized User

- By adding an authorized user to your credit card account, be aware that your use of that card may affect one another's credit, so if your child makes mistakes with that card, it could impact your score.

- You're responsible as the adult for paying the credit card bill, even if your young, authorized user spends up to the limit.

Example: Monica called her credit union and added her daughter, Erin, as an authorized user to her credit card account. Monica has good credit. When Erin buys a new laptop with the card, Erin can help pay for these charges, but Monica is ultimately responsible for paying any bills.

Monica can also remove Erin at any time. But Erin cannot remove Monica. Monica can see everything Erin charges. Monica receives credit for any cash-back, points or miles earned.

When Erin turns 18, as long as long as the card is well managed, it can contribute to a better credit score. However, a late payment or using too much available credit will decreases Monica's credit score and brings down Erin's score at age 18.

Debit Card

Although not a credit card, a debit card might be a good place to start with your younger teen before adding them to your credit card account as an authorized user. However, use caution, especially if you have a child who constantly loses things: A lost card could be a direct line to draining a checking account. (Note: Contact us immediately if your BECU credit or debit card is lost or stolen.)

A child or teen checking account often makes a debit card available for kids. BECU offers a free checking account that can be used by children or teens. A parent or legal guardian must be a joint account holder if the primary member is under 18 years old. A bank account is a good place for a first paycheck or babysitting money, to introduce the concept of saving (and interest earned) and not outspending your means. Think of it as training wheels for an actual credit card.

Note: The transaction is declined at point of sale if a minor attempts to use a BECU debit card and the transaction is more than their checking account balance. There are no overdraft fees for a debit card at BECU unless the member, who is over 18, has opted into the Optional Overdraft Service for Debit Card Transaction; however, NSF fees could still be incurred.

Pros of a Debit Card for Kids

- A debit card can help your child learn financial responsibility basics such as keeping a card in a safe, dependable location, staying within spending limits, how to use a card for purchases and how to check balances and monitor for fraud. Children who are 13 and older can have access to Online Banking.

- Typically, a parent or guardian must be a joint account holder until the child turns 18. So, you can keep an eye on their spending and ability to budget.

Cons of a Debit Card for Kids

- A debit card doesn't build credit or go on your child's credit history in the future.

- Best for ages 13 and older. Children can't access or view their accounts online or through a mobile app until they are 13, under the requirements of the Children's Online Privacy Protection Rule.

Prepaid Debit Card

Prepaid cards are another option. As the name suggests, you (or your child) load prepaid cards with funds. Your child then spends down the funds.

Pros of a Prepaid Debit Card for Kids

- Children of any age can use a prepaid debit card, and loading it with a small amount, such as $10 can help kids grasp how plastic works.

- Prepaid cards loaded with limited funds can help avoid larger losses that can come with a debit card.

Cons of a Prepaid Debit Card for Kids

- Tracking prepaid card spending can be challenging.

- Prepaid debit cards don't build credit or go on your child's credit history in the future.

- Prepaid cards don't offer some of the tools of a typical secured or unsecured credit card and aren't as great for "practice" as other options.

- If you lose a card, you cannot retrieve the funds. In addition, you'll likely face card fees for using the card.

Secured Credit Card

After your child turns 18, they may be ready for their own credit card, and a secured card might be a good introduction.

Many young people use a secured credit card to build a credit history. Your deposit (or "collateral") secures future charges with the card. Like a regular card, a secured credit card must be paid monthly as a minimum payment or in full.

Pros of a Secured Credit Card

- Builds credit like a regular credit card.

- You can only spend what you've deposited.

Cons of a Secured Credit Card

- Only available for those 18 and older.

- Your money is unavailable to you while in secure deposit.

- Late payments can damage your credit score.

Example: Your adult 18-year-old son uses $500 to secure the card; as a result, your son can charge up to $500. If he charges $100 in one month, he might pay it back over two months, at $50 each time.

Student Credit Card

Major credit card companies offer student cards aimed at college students and those with lower credit scores. A young adult still needs to show an income source, but student loans may count, depending on the issuer (call to ask). If your kids are looking for a student card, help them compare options, including points or miles for a rewards credit card, interest rates, fees and other details.

Remind them not to apply for cards too often, or they'll experience a credit score drop.

Pros of a Student Credit Card

- Builds credit history.

- If your adult teen doesn't have an income source, you (or another adult over 21) can co-sign or joint-apply for the credit card if the issuer allows it.

Cons of a Student Credit Card

- All the issues of any other credit card, including credit score drops due to overuse or late payments — remind your child to set up automatic payments to help avoid a forgotten bill.

- If you co-sign to help a teen get a student card, it's a risk for you as a parent. If your adult child doesn't repay that credit card debt, you're responsible — and unpaid bills can hurt both of your credit scores.

Kids and Credit Cards Q and A

At what age can a child get their own credit card?

Depending on the card issuer, your child must meet the company's minimum age requirement (generally 18) and show proof of independent income to demonstrate an ability to repay borrowed funds. The card's payment history and balances will then go on your child's credit report, which they can review. At BECU, a person must be 18, or a legally emancipated minor to apply for a credit card.

Will a child have their own credit card bill?

Typically, young adults may not have their own bills for authorized user credit cards. To teach financial responsibility, review your joint bill every month alongside your child. Once your child turns 18, some issuers will send a statement to your child. (BECU doesn't sent separate statements to authorized users.) If your child has a secured credit card or student credit card, they will receive the bill.

How do I get a credit card for my child?

If you hope to add authorized users to your account, call your bank or credit union to ask how the process works where children are concerned. After you add your child as an authorized user, your child will receive a credit card in the mail for activation and use. If you're the parent to a child over 18, co-signing on a child's credit card requires you to repay the balance, even if you didn't make any of the charges.

Should I co-sign a credit card for my child?

Don't co-sign unless you're willing to repay your child's debt in full, in addition to any late-payment charges or other fees. Remember that any bad credit outcomes around unpaid charges and late-payment fees will go on your credit history, as well.

What's the best way to build credit history for my child?

A good way to build credit history for a child under 18 may be through adding your child as an authorized user. After age 18, a secured credit card offers a good way to build credit through staying within a credit limit and paying bills on time.

Resources

Lora Shinn

Contributor