How To Budget as a Couple

Budgeting as a couple can improve your financial health and your relationship. Learn 10 steps to manage your money and reach your goals together.

Stacey Black

(She/Her/Hers)

BECU Lead Financial Educator

Updated Feb 22, 2024 in:

Budgeting

For couples, getting together to budget and manage your money can be good for your bank account and your relationship. According to statistics, financial disagreements can even predict divorce.

If you're in a solid financial situation, you might think you don't need to create a budget with your partner. However, going through the budgeting process can help you prepare for future uncertainty and help you tackle challenging times together. It can even be fun.

Follow these 10 steps for budgeting as a couple to help enhance your relationship, decrease arguments, help you manage money and accomplish shared goals.

1. Discuss Your Financial Values

If you're hoping to budget as a couple, diving right into a discussion with your partner about spreadsheets, budgets and paying debts can be a recipe for stress.

Instead, I recommend starting with a broader conversation about your financial hopes and interests. What type of lifestyle do you want? Do you want to buy a house? Understanding your individual and shared values can help you set goals and a budget you can both buy into.

From your conversations, you may find that you have different money styles. For example, one of you might be a spender, while the other might be a saver. In situations like this, consider setting individual goals in addition to your shared goals or setting up separate "spending accounts" for each person to use as they'd like.

2. Choose Financial Goals as a Couple — Starting With an Emergency Fund

Even if you and your partner have different money styles and goals, you can still find common ground and motivation if you set a few shared goals as a couple. These goals can bring you together for collaboration and help you get excited about your budget and stick to it for the long run.

Where do you start when you're setting financial goals as a couple? My advice is the same as it is for individuals: Set an emergency savings goal first. Your emergency savings total is your rainy-day cushion if you get laid off from a job, get a surprise medical bill or have an emergency home repair.

Common Financial Goals for Couples:

- Emergency fund

- Vacation

- Homeownership, including a down payment

- New car

- Home renovations

- Kids' college education

- Retirement

- Credit card debt

You can still have individual goals, too. For example, I might want to save money for a new car, but my boyfriend might want to save money for a trip home to visit his family. In this case, having individual savings and spending accounts for personal expenses might make sense for you.

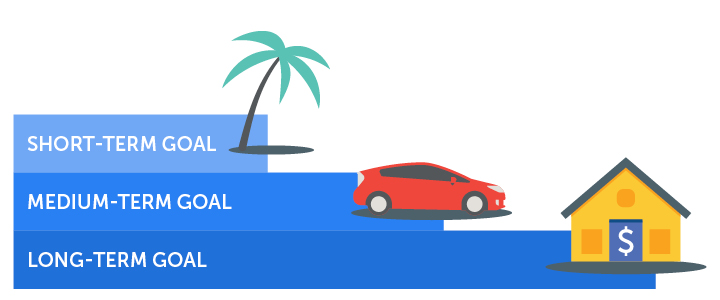

Map Out Short-Term, Medium-Term and Long-Term Goals

Your financial plan might involve just one goal, or it could have several. To best manage your money, map out whether your goals are short-term, medium-term or long-term. It may be easiest to start with one short-term goal, so you can enjoy the reward of reaching your goals sooner.

Examples of Short-Term Goals (Within the Next Three Years)

- Three to six months of emergency savings

- Vacation

- Back-to-school shopping

- Event tickets

Examples of Medium-Term Goals (Three to Five Years)

- No credit card debt

- New car

- Home upgrades

Examples of Long-Term Goals (Longer Than Five Years)

- Kids' college education

- Retirement savings

- Homeownership, including a down payment

- Major home remodeling

Estimate how much you'll need to reach your goal. Then divide that amount by how many months you think you'll need to save.

Example: Imagine you and your partner want to go on a two-week vacation together next year. You estimate the trip will cost $5,000 total. Divide the total amount you need to save by 12 for the number of months in a year to determine that you need to save $417 per month.

Of course, you could also save $2,500 separately. But working on a joint goal — perhaps even in a joint savings account — can provide encouragement and accountability. Even on a tight budget, make room for time off. There are dozens of low-cost, local vacation options in Washington, for example, that are perfect for couples and families.

3. Add Up Your Combined Income

Now that you know what you want to save for, figure out together how much money you have for reaching your shared goals.

Add up each person's net income (the amount after income tax withholding, also known as take-home pay) from all sources, including wages, salary, freelance and side-gig income.

This is the total amount of money you have for essential and discretionary spending and savings, individually and as a couple.

4. Track Your Expenses

Make a detailed list of your expenses — yours, theirs and shared — all in one place. You might need to track your expenses for a month or two to clearly understand where you spend your money.

List everything you pay for, including automatic bill payments, digital subscriptions, online purchases and in-store payments. Be sure to include periodic expenses — those that don't occur monthly — like annual dues, insurance payments, haircuts and holiday gifts.

You can track expenses with a notebook and pencil, use a spreadsheet or choose from various online tools. BECU members can use Money Manager, for example. The best tool is the one that works for you.

5. Categorize Your Spending

Review your expenses with your partner after tracking your spending for a couple of months. Group similar purchases into categories, like housing (mortgage or rent), groceries, transportation and entertainment.

Some expenses are essential, like paying for housing and utilities. Others might not rise to the level of "essential," but they may be necessary to one or both of you. Try not to pass judgment on how important expenses are at this point, especially if something is more important to you than it is to the other person.

For example, a premium cable package might be the only way to watch your favorite sports, but your partner might not be into sports. The point of this part of budgeting as a couple is just to get everything out in the open so you can see where your money is going. Prioritizing expenses comes next.

6. Compare Income to Expenses

After totaling your monthly expenses, subtract that number from your net monthly income. If, after adding everything up, you have money to spare, then creating a budget as a couple will be pretty straightforward.

But if, like many people, your income is less than your expenses, the next steps will likely be more challenging because you'll have to figure out where to cut back.

7. Prioritize Expenses and Cut Back as Needed

Keep an open mind and look at everything you spend money on. Go line by line. Respect what the other person wants, even if it's not important to you.

This is an excellent time to think about whether you want all your expenses to be pulled from a joint account or if there are some things you want to cover individually. You can choose from several methods to split bills as a couple, such as splitting everything 50-50 or basing your share of expenses on your percentage of household income.

You can also determine how much you need in a joint versus individual account. After covering the essentials, decide how to manage the fun stuff.

Don't forget about less frequent, upcoming expenses like insurance and taxes. If you know you'll need to come up with $1,400 for auto insurance or property taxes in a year, save enough every month to cover the bill when it's due.

8. Choose a Budget Method That Works for You

Remember, a budget is a projection of how you'll spend and save money each month. There are many different budgeting methods available. If you choose a method that doesn't work well for both of you, you can always try a different one.

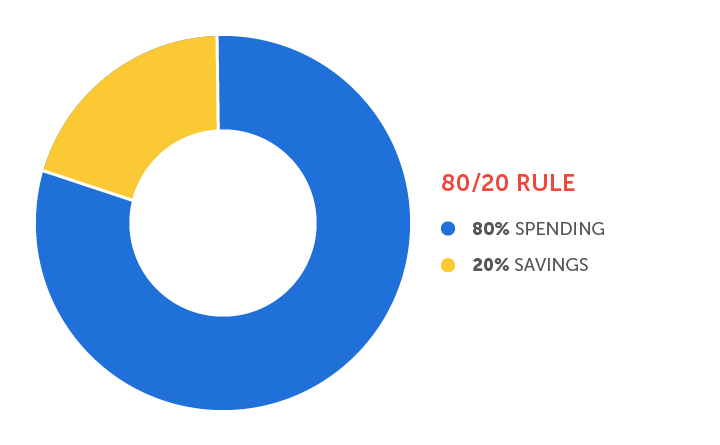

80/20 Rule

This strategy might benefit you if you're new to budgeting as a couple. For your joint income, you can spend 80% on needs and wants and commit 20% to savings. This 20% could go toward emergency funds, college savings, retirement savings or debt reduction. Be sure to prioritize your emergency savings first.

If you're currently spending 90% or even 100% on your joint needs and wants, try to cut back in a category so that you can put 20% toward your savings goals.

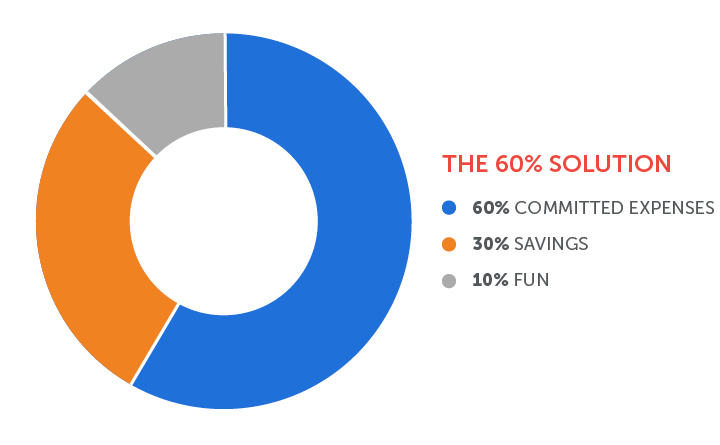

The 60% Solution

This budget approach can be great for couples because it commits you to a slightly higher savings amount than the 80/20 Rule, and it leaves room for you and your partner to spend on fun things for both of you.

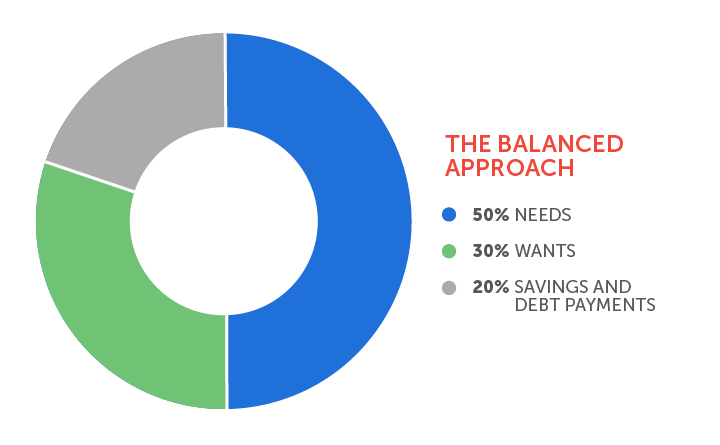

The Balanced Approach

This could be a good option if you and your partner are trying to pay off debt. You'll have to be a little more specific than the two previous methods about identifying which expenses are essential (needs versus wants), and you'll need to agree on your debt reduction method while still committing to saving if you can, even if it's a small amount.

Other Budget Options

You can be as general or detailed as you want in your budgeting based on your financial situation and how much time and effort you want to put into it.

If you like to get into the details and have aggressive savings goals, you might like zero-based budgeting, where every dollar is accounted for and given a purpose.

Caution: If you're detail-oriented, be careful not to let your budgeting habits become a source of frustration for your partner, especially if you have different money styles. Help each other stay on track but give each other space to spend money on what matters to you individually.

9. Check In: Make Sure You're on the Same Page

Communication and understanding will be key in the budgeting process. I recommend scheduling a financial review once or twice a month, but you can make it fun — like a date night. As you become a pro at budgeting, you can move to quarterly reviews.

Pour yourselves your drink of choice, make a later dinner reservation or cue up your favorite movie. Booking your financial check-ins as a fun date-night activity can make them less tedious and more enjoyable.

First, try touching on lighter, optimistic topics that bring you together like financial goals. Then begin diving into the nitty-gritty of things like debt, monthly income, savings accounts, financial goals and budgeting aspirations. How close are you to your budget? Have your financial goals changed? In time, your budget night could become an aspect of your relationship you look forward to.

Tip: For relationship-building exercises, write down financial conversation starters or questions to prompt money memories and put them in a bowl or dish. Pull one out to ask your partner during your review dates. A few ideas:

- What was your family's attitude toward money?

- Did you have an allowance?

- Did your parents save for their retirement? Why or why not?

- Were there any money stress points when you were growing up?

- If you won $1 million, what would you do? $10 million?

- What did you want to buy for yourself when you were a child?

10. Track Your Progress

Once a year, do a holistic review of your expenses and spending — as if you're just beginning your budget process — to ensure the numbers still work for you.

It's Never Too Early or Too Late To Start

Whether you're a new couple or you've been together for years, budgeting with your partner can help you reach your financial goals and deepen your relationship. Keep the lines of communication open and give each other time and space to learn and grow.

Resources

Related Content

Note: Where examples are used, the products, rates and returns are not guaranteed and are for educational purposes only. The information and examples are not advice and may not reflect the rates, products or services currently available from BECU. BECU does not offer or guarantee products or rates in this article.

Stacey Black

(She/Her/Hers)

BECU Lead Financial Educator